Extra large demand charge - network tariffs 101

The value stack breakdown continues

One of the first and most important decisions you’ll make as a battery developer is where to put the goddamn thing. A major driver behind this decision is network costs (especially demand charges). In this post, we will cover the basics for you because we’re just such lovely people.

For the purposes of this post, we will focus on batteries with co-located load. However, if you’re a developer building without co-located load, the information here will still be valuable to you, as you underestimate network costs at your peril.

What’s the deal with bills?

At a high level, the components of your electricity bill that you can control are -

Consumption (kWh) - you are charged for the electricity you consume over the billing period. This cost is levied both by your retailer and by your distribution network service provider (DNSP), with both being billed by your retailer.

Demand (kVA) - you are also charged for the demand you place upon the network infrastructure to which your site is connected. The way this is calculated varies by DNSP. Each of the NEM’s 13 DNSPs has a different cost base, driven by geography, climate, infrastructure, customer base and demand profile.

There are other components to a bill too but you don’t really have control over them beyond changing your consumption, and they don’t tend to be a material source of cost anyway.

DNSPs are responsible for setting their own network tariff structures and prices to recover the costs of providing network services to your site. The costs and incentives you face will either be a bearable cost of doing business or a critical part of your business case.

Whilst we will also be discussing general concepts here, our focus in this post will be non-residential, distribution-connected, unscheduled batteries.

Let’s start with the basics.

Network component – what costs is this recovering?

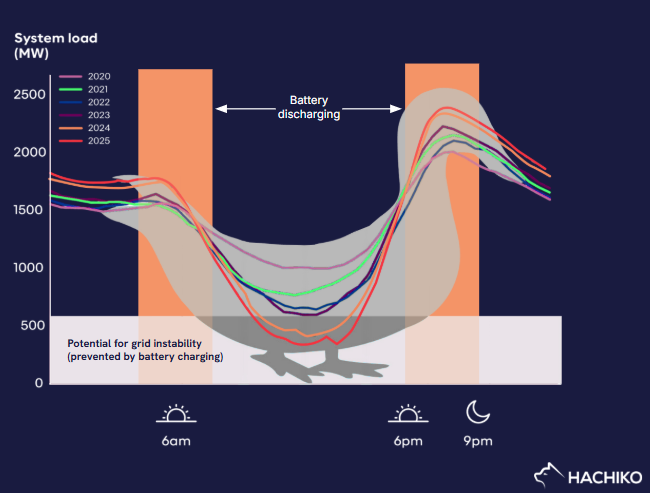

Electricity is defined as an essential service in Australia, and so our network businesses have to make sure it can be delivered to consumers, with high demand days being the biggest historical challenge (although low demand is becoming a big problem now too).

Hachiko made that. It’s not a dog though, it’s a duck.

Consequently, our networks are built to support very high levels of electricity demand, even if those very high demand periods only occur a handful of times a year. Network businesses invest in, build, and maintain a lot of capital-intensive, long-lived assets. All this costs money, and ultimately consumers foot the bill.

The network component of an electricity bill recovers all the costs associated with building, operating and maintaining the NEM’s transmission and distribution networks. This includes everything from poles, wires and transformers, to the people the network businesses employ and the desks they sit at.

As you might expect, that sh*t is expensive.

The charts below are a couple of years old but give a sense of just how much distribution network stuff there is out there, and how much it’s all worth.

Source: AER

The regulatory asset base (RAB) represents the total remaining value of all DNSP-owned assets to fulfil network obligations. The RAB is recovered from connected customers over time through depreciation. As the charts above show, the total RAB for all the NEM’s DNSPs was nearly $90 billion at 30 June 2023. Add in the ~$26 billion of transmission network RAB, and the costs of transmission yet to be built, and you’ve got some pretty big costs to recover from just 11 million customers.

Now you know why everyone was furious about this.

How are these costs recovered?

The NEM has 13 DNSPs, all of which are monopolies with their own patch to service. All are highly regulated by the Australian Energy Regulator (AER) to ensure that they don’t overbuild or overcharge customers for their services.

We won’t go into the details here, but the short version is, the AER will determine how much revenue each DNSP is allowed to recover from its connected customers in a regulatory control period (typically five years). Depreciation of the RAB is just one cost that is included in this determination. It also includes DNSP opex and returns for their shareholders/lenders.

Once the revenue requirement is set, DNSPs determine how they will recover this revenue from customers. The first step in this process is the development of a tariff structure statement, which is set for each regulatory control period.

A tariff structure statement sets out the tariffs a DNSP will make available in a regulatory control period, how each of those tariffs will be structured, and what types of customers will be assigned to which tariff.

Typical components of a network tariff

The structure of a network tariff relates to which of the following four typical components are used, how those components are measured, and any time windows associated with the components.

There are other component types used, including metering service charges and capacity charges, but we haven’t bothered covering those here because we’re flat out mate.

There aren’t any hard and fast (or strong or…bett?) rules around what costs a DNSP can recover via which tariff component. It’s up to each DNSP to design and price their tariffs in a way that ticks the relevant compliance boxes and enables it to recover its costs.

What a banger factory these guys are

Prices and incentives

Now that they’ve set the tariff structure, it’s time to add prices. DNSPs develop tariff structures that apply for five years but prices are set yearly. This is done through their annual price lists, which are publicly available.

Most C&I customers will have unbundled bills, clearly showing the network pricing components alongside their retail pricing offer. This gives businesses useful information if they want to install a battery, as they’ll be able to see how to optimise network tariff costs/value against other available value streams.

The concept of C&I sites trying to minimise demand charges has been around for a long time. They have tended to:

Shift their peak load (i.e. grid import) from a more expensive time to a less expensive time (not that common without on-site generation/batteries); or

Reduce load (i.e. grid import) during peak demand charge periods (sometimes referred to as ‘peak-shaving’ or ‘peak-lopping’). This is either done by curtailing load or switching to on-site generation/storage.

When combined with actual prices, different tariff structures send different economic signals to customers and drive different behaviours.

I’m particularly proud of this table.

Tariff structures have changed a lot over the last 10 years, largely due to a policy decision that required DNSPs to move toward cost reflective network tariffs. Traditional flat or volumetric network tariffs did not accurately reflect the drivers of network costs (e.g. buildout to meet peak demand) and led to cross-subsidisation across electricity users. The underlying principle of cost reflective network pricing is that customers who place greater demands on the network—and thereby drive up costs—should contribute a larger share toward those costs.

Can I pick my tariff?

As a general rule, customers are assigned to a specific network tariff when they connect to the network. Most tariff structure statements and price lists will include decision trees to easily determine your default tariff, often based on the voltage of the line you are connected to and your annual consumption or demand. However, C&I customers do have some influence over which tariff they are assigned to, and may be able to negotiate something bespoke.

As we’ve shown, network tariff prices are adjusted every year, but underlying tariff structures are only updated every 5 years. That’s a long time to be stuck on a bad tariff. This highlights just how important it is to fully work through the impact of your network tariff on your trading strategy and overall business case.

Good tariff, bad tariff

Each DNSP has control over what tariffs it offers, so there are big differences in what’s on offer between the 13 DNSPs. Anyone in the battery game will have a view on which DNSPs have good or bad network tariffs.

We’ve pulled out one “good” tariff and one “bad”, for C&I customers with storage, below.

Also, the ‘all other months’ component applies from 7am-7pm on business days. That is a hell of a window. Unless you have a pronounced peak in your load profile which can be offset by a BESS, you’re pretty cooked here.

Whilst this looks similar on paper to the Powercor tariff, the monthly numbers are much lower, the peak year structure biases more towards the evening (which helps C&I businesses who may down tools at ~7pm), and the all-year structure is a bit more forgiving (30-minute intervals instead of 15).

Most large business tariffs are weighted toward the demand charge component. So, the best tariffs are those that provide sufficient opportunity to reduce/shift your demand away from the demand charge periods. As a reminder, network costs tend to make up a significant proportion (~40-60%) of your electricity costs.

In both cases, demand charges are set on a rolling 12-month basis. This means that if you draw a large amount of power from the grid during a peak window—even just once—it can impact your charges for many months afterward.

If you can bring your demand charges down, including through the use of a battery, there is potential to make significant savings. DNSPs are now starting to develop battery-specific network tariffs (mostly for standalone BESS) to incentivise the behaviours that influence network stability positively, and dis-incentivise those that do the reverse.

So what do I do?

You can’t participate in energy/FCAS markets if you are not grid-connected, and you can’t escape network costs if you are grid-connected. So you have to get on board.

Get in, losers, we’re going to maximise revenue from the value stack

However, that doesn’t mean pain is a pre-requisite.

In summary:

For developers building batteries (+ PV) with no co-located load -

Network costs represent a material but mostly bearable cost of doing business.

Some network tariff structures create costs that render most projects unviable, so developers are smart about where they locate their projects.

For developers building batteries at C&I sites -

Ability to reduce/minimise demand charges presents a significant source of value for their customer/landlord (the C&I site owner).

It therefore tends to represent a big and, more importantly, predictable part of the business case.

It is big because network costs typically make up 40-60% of the customer’s total electricity cost.

It is predictable because the major drivers are the customer’s load profile and a tariff structure which, as you have seen, does not change very often.

For both of the above - factoring network costs (especially demand charges) into your overall operational strategy is a must. Make sure you choose your optimisation/operations partner wisely, because even a small f***-up could leave you with a big bill and many unhappy investors/customers for a long time to come.

If you want to chat about this, you know where to find us. Thanks for reading!